Research shows how markets respond when firms back environmental and social commitments with rigorous disclosure

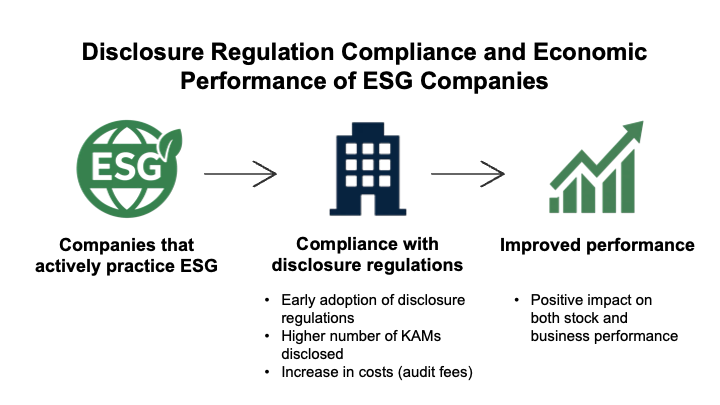

Companies with strong environmental, social, and governance (ESG) track records performed better than their peers after being required to adopt more rigorous auditing standards. This is according to a new study from researchers at Nagoya University, which is the first to examine the connection between the implementation of “key audit matters” (KAMs) and firms’ sustainability practices.

ESG stands for environmental, social, and governance—a framework for evaluating how companies manage environmental impacts, treat stakeholders, and maintain ethical oversight. Companies with strong ESG practices demonstrate long-term commitment to sustainability and social responsibility. Investors increasingly view these commitments as an important signal of corporate quality.

In 2015, the International Auditing and Assurance Standards Board (IAASB) recommended that auditors communicate KAMs, the most significant issues identified during an audit, to better inform investors about company risks. Although Japanese firms with high ESG scores tended to pay higher fees for auditing and related consulting services after the implementation of KAMs, they also performed better in both accounting and market indicators.

“You can’t simply buy credibility by paying for expensive audits,” clarified co-author Hu Dan Semba, Associate Professor at Nagoya University’s Graduate School of Economics. “But if you’ve demonstrated commitment to sustainability practices, then investing in more transparent auditing amplifies that credibility, and markets reward it.”

As more countries adopt similar standards, the research offers insights into which companies are likely to benefit the most from transparency requirements. The results were published in Managerial Auditing Journal.

A transparency experiment in Japan

The case of Japan provides a unique scenario for studying the implementation of stricter auditing standards. Publicly traded companies were given the option to voluntarily adopt KAMs early in fiscal year 2019, before the practice was made mandatory in fiscal year 2020. This created a natural experiment for exploring the motivations behind corporate behavior.

The research team, led by Semba and co-author Maretno Agus Horjoto of Pepperdine University, analyzed 1,065 Japanese firms from 2009 through 2023, tracking which companies adopted transparency requirements early, what it cost them, and how they performed afterward.

Twenty-four non-financial firms volunteered for early adoption, and the analysis showed that the decision to volunteer was positively related to a firm’s ESG score. “These companies stepped forward when they didn’t have to,” Semba noted, “demonstrating their interest in signaling their underlying quality.” However, sustainability-focused companies also tended to pay more for auditing and non-auditing services compared to their peers. These costs reflect more rigorous examinations and additional advisory work to address issues identified during audits.

The researchers, citing scholarship on Japanese business culture, suggest that this willingness to voluntarily embrace transparency may reflect the influence of “sanpō-yoshi.” This principle, developed by the Ōmi merchants between the 16th and 19th centuries, holds that transactions should benefit the seller, the buyer, and society.

Interestingly, the results also showed that early adopters paid lower audit and non-audit fees after reporting KAMs became mandatory. This implies that these companies were able to use the pilot period as a chance to disclose and mitigate audit risks.

Market response to audit transparency

Despite the additional costs, companies with higher ESG scores had better accounting and market performance on average in the years following mandatory KAMs implementation (2020-2023). While there is some evidence that the stricter standards increased firm performance overall, this effect was amplified for firms committed to sustainability and social responsibility. A high-ESG company tended to have higher stock returns and a better return on assets (ROA)—how profitable a firm is in relation to its total assets.

As the use of KAMs spread globally, these findings suggest that companies with established ESG practices are likely to receive the most benefits from more transparent auditing standards. “The market appears to view ESG practices and KAMs reporting as a sort of two-factor authentication,” explained Semba. “When companies with authentic sustainability practices invest heavily in transparent auditing, investors interpret it as credible signal of organizational strength.”

Publication

Maretno Agus Harjoto and Hu Dan Semba. (2025). Sustainability and financial disclosure: Role of ESG in key audit matters adoption. Managerial Auditing Journal, 1-38. https://doi.org/10.1108/MAJ-01-2025-4663

Funding

This research was supported by the Tsao Family Foundation and JSPS KAKENHI Grant Number JP22K01808.

Media contact

Alexander Evans

International Communications Office, Nagoya University

icomm_research@t.mail.nagoya-u.ac.jp

Expert contact

Hu Dan Semba

Graduate School of Economics, Nagoya University

ko.tan.n8@f.mail.nagoya-u.ac.jp

Top image

Researchers found that companies with strong sustainability practices benefit more from audit transparency. Markets appear to reward authentic commitment backed by rigorous disclosure. Credit: Kano Okada, Nagoya University